How to Create a Retirement Plan [Step by Step]

Understanding Your Income

A crucial first step in assessing your financial situation is to thoroughly understand your income streams. This involves not just your salary or wages, but also any other sources of revenue, such as investments, side hustles, or freelance work. Detailed records of all income sources, including dates and amounts, are essential for accurate budgeting and financial planning. Careful consideration of irregular income sources, like seasonal bonuses or commission-based pay, is also important for long-term financial stability.

Analyzing Your Expenses

Equally important to understanding your income is meticulously analyzing your expenses. This includes categorizing all your spending into essential (housing, utilities, food) and discretionary (entertainment, dining out, shopping) categories. Tracking your expenses for a specific period, such as a month or a quarter, provides valuable insights into spending patterns and areas where potential savings can be found.

Evaluating Your Assets

Identifying and evaluating your assets is a key component of assessing your overall financial health. This includes tangible assets like property, vehicles, and valuable possessions, as well as intangible assets such as investments in stocks, bonds, or mutual funds. A clear inventory of your assets helps you understand your current financial position and potential investment opportunities.

Assessing Your Liabilities

Alongside your assets, understanding your liabilities is critical. This encompasses all your debts, including mortgages, loans, credit card balances, and outstanding bills. Accurate record-keeping and understanding the interest rates and repayment schedules associated with each liability are essential for effective debt management and financial planning. A comprehensive overview of your debts helps to prioritize repayment strategies.

Identifying Savings and Investments

Evaluating your savings and investment accounts is vital for assessing your financial health. This includes examining the balances in savings accounts, checking accounts, and any retirement accounts like 401(k)s or IRAs. Understanding your investment portfolio, including stocks, bonds, and other assets, provides a clear picture of your financial resources available for future needs and goals.

Determining Your Financial Goals

To effectively assess your financial situation, you need to define your short-term and long-term financial goals. What do you want to achieve financially in the next year? Five years? Ten years? These goals can include buying a house, paying off debt, saving for retirement, or funding your children's education. Clearly defined goals help provide a roadmap for your financial decisions.

Creating a Budget

A crucial step in understanding and managing your finances is creating a budget. A budget outlines your expected income and expenses, allowing you to track your spending habits and identify areas where you can save or cut back. Creating a detailed budget, which takes into account your income and expenses, is essential for effective financial management and helps you to achieve your financial goals.

Developing a Savings and Investment Strategy: Fueling Your Future

Understanding Your Financial Goals

Defining your financial goals is crucial for developing a successful savings and investment plan. Think about what you want to achieve in the short-term, such as saving for a down payment on a car or a vacation, and what you aspire to accomplish in the long-term, like retirement or funding your children's education. These goals will serve as your guiding principles and help you prioritize your financial decisions.

Clearly outlining your financial objectives will provide a roadmap for your savings and investment strategies. This will allow you to focus your efforts on achieving your desired outcomes and make informed choices about where to allocate your resources.

Assessing Your Current Financial Situation

Before diving into savings and investment strategies, it's essential to understand your current financial situation. This involves evaluating your income, expenses, debts, and existing assets. A thorough assessment will provide a clear picture of your financial standing and help you make realistic and achievable savings and investment plans.

Thoroughly analyzing your current situation will help you identify areas where you can cut costs and improve your financial position. This detailed analysis will also help you determine the amount you can comfortably save each month and the risk tolerance you can afford, which are critical in developing an effective investment strategy.

Creating a Realistic Budget

Developing a budget is a fundamental step in managing your finances effectively. A budget outlines your income and expenses, allowing you to track your spending habits and identify areas where you can reduce costs. This will help you allocate funds towards your savings and investment goals.

A well-structured budget is essential for achieving financial stability and provides a clear picture of your financial health. It helps you visualize where your money is going and enables you to make informed decisions about your spending and saving habits.

Choosing Appropriate Savings Accounts

Selecting the right savings accounts is critical for growing your funds. Consider factors such as interest rates, minimum balance requirements, and fees when comparing different options. Different accounts cater to various needs, so researching and comparing is vital.

High-yield savings accounts can provide a higher return on your savings compared to traditional accounts. This can significantly impact your long-term savings goals and help you accumulate your funds more effectively.

Exploring Investment Options

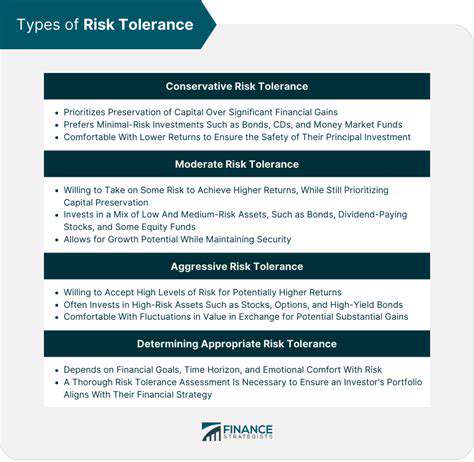

Once you have established a solid savings foundation, you can explore various investment options. Research different investment vehicles, such as stocks, bonds, mutual funds, and real estate, to determine which ones align with your risk tolerance and financial goals. Understanding the potential risks and rewards associated with each option is crucial.

Diversifying your investments across different asset classes is a crucial aspect of wealth creation. This approach can help mitigate risk and enhance potential returns over the long term.

Monitoring and Adjusting Your Plan

Developing a savings and investment plan is not a one-time event; it's an ongoing process that requires regular monitoring and adjustments. Track your progress towards your goals, review your budget, and re-evaluate your investment strategy periodically. This will allow you to adapt to changing circumstances and stay on track to achieving your financial aspirations.

Regularly reviewing and adjusting your savings and investment plan is crucial for staying on track with your financial goals. Life events and market fluctuations can impact your financial situation, so adapting to these changes is essential for long-term financial success.

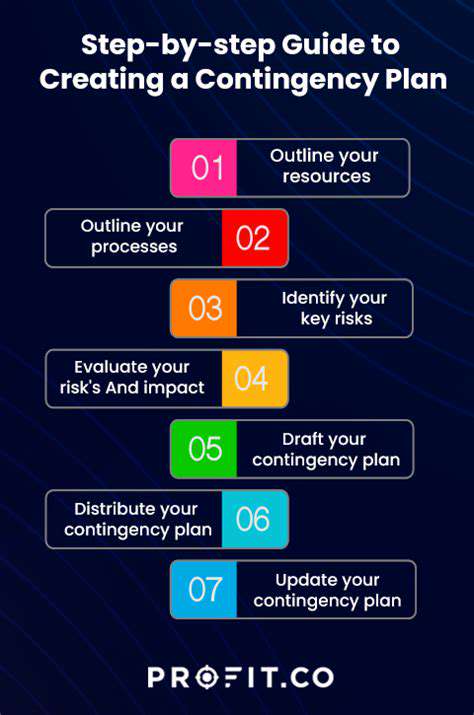

Contingency Planning: Preparing for the Unexpected

Contingency Planning Fundamentals

Contingency planning is a crucial aspect of risk management, designed to anticipate and mitigate potential disruptions to an organization's operations. It involves developing proactive strategies to address unforeseen events, from natural disasters and cyberattacks to supply chain disruptions and economic downturns. Effective contingency planning can significantly reduce the impact of these events and help maintain business continuity. A well-defined plan ensures that critical functions and resources can be quickly restored, minimizing financial losses and reputational damage.

Properly executed contingency planning involves identifying potential risks, assessing their likelihood and impact, and developing specific procedures to respond to them. This process requires careful analysis of internal and external factors, including technological advancements, economic conditions, and regulatory changes. Understanding your organization's vulnerabilities and dependencies is paramount to creating a robust contingency plan.

Identifying Potential Disruptions

Identifying potential disruptions is the first step in developing a comprehensive contingency plan. This involves a thorough risk assessment, evaluating various scenarios that could affect your organization's operations. Consider factors like natural disasters, geopolitical instability, technological failures, and supply chain issues.

Analyzing potential disruptions requires a systematic approach to identify potential vulnerabilities. This often involves brainstorming sessions, reviewing historical data, and consulting with experts in various fields. The goal is to anticipate a wide range of possible disruptions, not just the most likely ones.

Developing Response Strategies

Developing response strategies is a critical component of contingency planning. This involves creating detailed procedures for each identified disruption, outlining specific actions to take before, during, and after an event. These strategies should encompass operational procedures, communication protocols, and resource allocation plans. Implementing these strategies requires clear communication and coordination among all stakeholders. A well-defined strategy ensures that everyone understands their role in the event of a disruption.

Detailed response strategies should include specific actions for different levels of disruption severity. This allows for a flexible and adaptable approach, enabling swift and effective responses to changing circumstances. This also helps to ensure that resources are allocated appropriately based on the specific nature of the disruption.

Testing and Evaluating the Plan

Testing and evaluating the contingency plan is essential for its effectiveness. Regular drills and simulations help ensure that procedures are understood and executable. These tests also identify weaknesses and gaps in the plan, allowing for improvements before a real-world event. Regular review and updates are essential to maintaining a relevant and effective plan.

The success of a contingency plan depends on its ability to withstand real-world testing. Therefore, it's important to conduct regular exercises to practice the plan and identify potential areas for improvement. This will help ensure the plan is not only comprehensive but also practical and executable. Realistic simulations can highlight areas needing adjustment, thereby improving the overall response strategy.

Implementing and Maintaining the Plan

Implementing the contingency plan requires clear communication and coordination among all stakeholders. This involves training staff on procedures, providing necessary resources, and ensuring effective communication channels are in place. Effective communication is vital during a crisis, allowing for seamless coordination and timely responses.

Maintaining a contingency plan is an ongoing process that requires regular reviews and updates. This ensures that the plan remains relevant and effective in the face of evolving threats and circumstances. Regular assessments of the plan's effectiveness and adjustments based on new information are essential to its long-term viability.

Read more about How to Create a Retirement Plan [Step by Step]

![Best Health Insurance Plans for Families [2025]](/static/images/30/2025-05/EvaluatingCoverageandBenefits.jpg)

![Best Retirement Income Strategies [Generating Cash Flow]](/static/images/30/2025-07/RealEstateInvestmentTrusts28REITs29forPassiveIncomeandGrowth.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt